TOMYPAK recently released their Annual Report 2015 and their 2016 Q1 results. Some studies had been done on the recent Annual Report and also the Q1 report. Previously, i had posted on

TOMYPAK[1]. This will be the updated information on TOMYPAK. Let's go:

1) Fundamental Analysis:

|

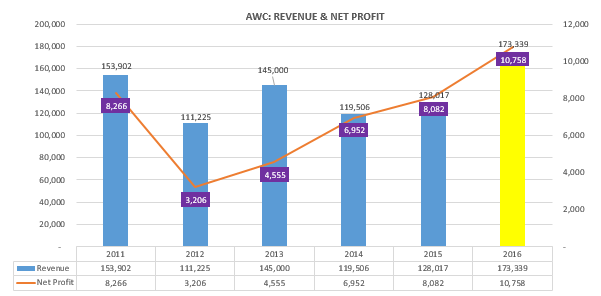

| TOMYPAK Q1 2016 Result |

Both revenue and net profit of q-o-q had decreased 1.43% and 34.07% respectively[2]. For me, the results are within expectaion, but the share price on 19 May 2016 shows another story. From the volume, a lot of shareholders are quite disappointed with the result. Main reasons of the net profit drop were due to:

i) Slight reduction in demand from overseas customers

ii) Increased cost of production arising from increased cost of imported raw material

iii) Higher energy and labour cost

iv) Foreign exchange volatility

|

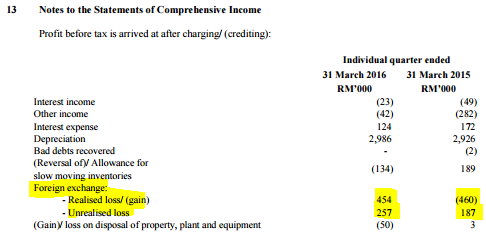

| Impact of Foreign Exchange Volatility |

I will further elaborate on the reasons. Demand from overseas reduced 6% and 13% respectively for q-o-q and Q4 Result. Demand from locals increased 4% and reduced 4% respectively for q-o-q and Q4 Result. The cost of imported raw material increased due to the oil price had rebounded. Remember that the raw material of plastic is crude oil. When the price of crude oil increased, thus the cost production also increased. Higher energy and labour cost is because of the new foreign worker levies charges implemented by the government[3]. As for the foreign exchange volatility, this is something that we need to take note for the export-oriented companies earning USD. In Q1 2015, TOMYPAK had realized gain for the foreign exchange but for this Q1, it had a realized loss of RM454k. Although the amount is just minor, however, we need to take note of this line item. Despite with the setbacks, TOMYPAK management is still optimistic as the food and beverage sector remains resilient. Like my friend say, no matter how bad the economy was, people will still eat Maggi. In fact, more people will eat Maggi at that time, and TOMYPAK provides plastic packaging for Maggi~ haha.