OCNCASH posted a WOW-ing result today (25 November 2015), well at least for me, it is a WOW. Let's go through the Quarterly Result.

1) Fundamental Analysis:

{kind=link}

|

| OCNCASH Q3 2015 Result |

A point to note here, if we compare the cumulative Q3 2015 against 2014 annual result, the net profit had already exceeded 2014 annual result by 44%. This is just the Q3. I think roughly we will know what will be happening in Q4. And how the result will impact the price, especially when the chart had broken a historical new high. This is what we call a growing company. Just to recap, OCNCASH is specialized in felts division and nonwoven division[1].

|

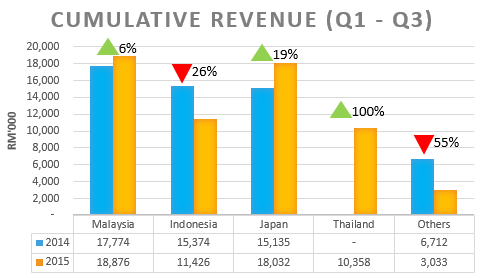

| Cumulative Revenue by Geographical Segment |

Remember in my previous post, in the annual report, Mr Chairman assured the nonwoven division will have a double digit growth this year. The increment of 9.76% in revenue for nonwoven industries on quarter on quarter basis is mainly due to increase in sales to Thailand and Japan. Revenue from air condition market also recorded an increase. The air condition is the mask industry, remember the haze that happened in Malaysia and Indonesia during September and October. However for the felts division, Indonesia showed a decrease in revenue due to the slowdown in new automotive sales. New factory will be completed in June 15 in Indonesia. That's why we see the liabilities increased for the felts division, it is all for the expansion of the business in Indonesia.

|

| Page 6 of Q Result |

In terms of fundamental, the company had no problem at all. It is expanding its plants in Indonesia and the sales of nonwoven industry is high in Thailand and Japan. With such pace, i think the company might be net cash in a year or two. OCNCASH also announced a dividend of 0.7sen which will ex on 8 December 2015, which is around 2 weeks more from now.

2) Technical Analysis:

But for me, personally, i will wait again for the chart to break new high, reason being:

1. The cumulative 3 quarters net profit had already exceeded last years full year, with new factory fully operating in Q1, 2016.

2. My entry price is low, and i will be waiting for the last Quarter, no matter how bad the result is, it will still be pushed up due to its low price with strong fundamental and net profit margin.

3. Theme play of transfer to Main Board. Take a look at the example of HHGROUP, once they announce that they wanna apply for Main Board, notice how HHGROUP flies...

Summary:

OCNCASH for me is still an OCEAN full of CASH. It is my STAR STOCK of 2015.

- A whooping 3 digit growth of NET PROFIT 600%

- New factory in Indonesia and expected to pump in profit at Q1, 2016 for Felts Division

- Good sales from Thailand and Japan for the Nonwoven Division.

- Only announced 3 quarters of result, but the net profit had already overtaken last year's full result by 44%.

- 69% of the net profit generated from overseas, earning USD.

- Ex-date for the 0.07sen dividend is on 8 December 2015.

- Broke historical new high and will be continue to challenge the resistance of 0.46, after that, sky is the limit.

- Eligible to transfer to Main Board. This might be another theme play for OCNCASH.

- Low price with good fundamentals, a possible target for market makers to push. If your price is low, you can continue to hold.

- Stay calm and wait for the fruit to ripe

- You can always refer to my post http://gainvestor10sai.blogspot.my/2015/09/ocncash-ocean-full-of-cash.html

- New factory in Indonesia and expected to pump in profit at Q1, 2016 for Felts Division

- Good sales from Thailand and Japan for the Nonwoven Division.

- Only announced 3 quarters of result, but the net profit had already overtaken last year's full result by 44%.

- 69% of the net profit generated from overseas, earning USD.

- Ex-date for the 0.07sen dividend is on 8 December 2015.

- Broke historical new high and will be continue to challenge the resistance of 0.46, after that, sky is the limit.

- Eligible to transfer to Main Board. This might be another theme play for OCNCASH.

- Low price with good fundamentals, a possible target for market makers to push. If your price is low, you can continue to hold.

- Stay calm and wait for the fruit to ripe

- You can always refer to my post http://gainvestor10sai.blogspot.my/2015/09/ocncash-ocean-full-of-cash.html

Let's Ride the Wind and Gainvest

Gainvestor 10sai

26 November 2015

12.25am

Sources:

[1]:http://gainvestor10sai.blogspot.my/2015/09/ocncash-ocean-full-of-cash.html

[2]: Q13 2015 Report

[2]: Q13 2015 Report

No comments:

Post a Comment